Founded in 2008 and starting out as an online-only player in 2010, the company entered offline retail in 2013 and has since scaled to 2,067 stores across India. In a highly fragmented market, Lenskart stands out as a rare consumer-tech venture that has built both scale and market leadership.

Here’s a look at five strengths driving its story—and the risks investors should watch out for.

Growth: Seeing a future

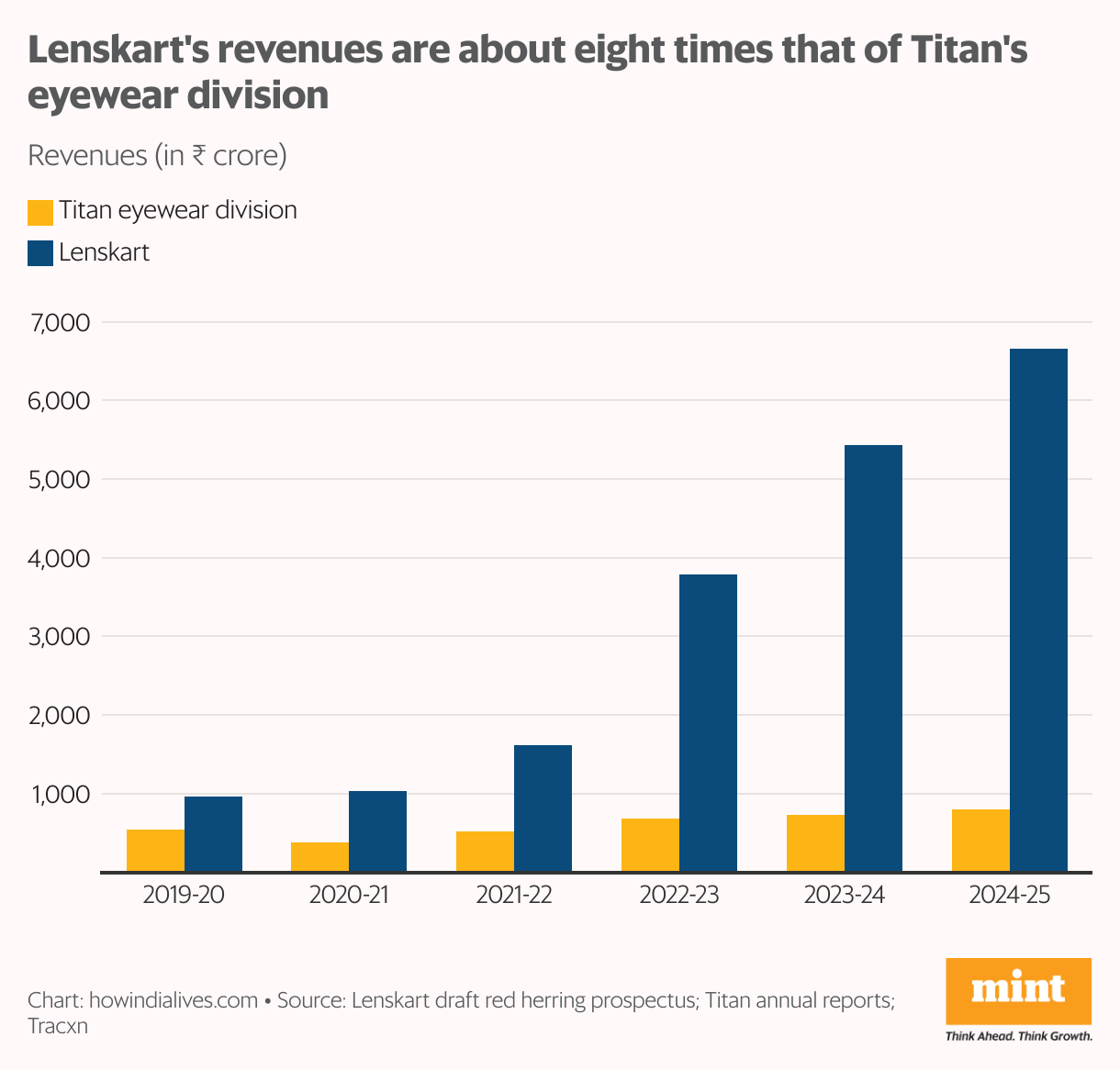

When Lenskart entered the eyewear market, the space was fragmented and dominated by scattered local players. Titan had already launched its Eye+ division in 2007, but the category remained a small piece of its larger jewellery-led empire.

Lenskart, starting later, quickly overtook Titan Eye+—its revenues were already 1.8 times bigger in FY20 and had surged to 8.3 times by FY25. The company’s edge came from a hybrid strategy of online accessibility and offline reach, backed by heavy investment in a vertically integrated supply chain that spans design, manufacturing, and retail.

Profitability: Wider outlook

Spotting potential beyond India, Lenskart exported its value-for-money, tech-enabled model to global markets—expanding largely across Asia, at times through acquisitions.

Its biggest move came in 2022 with the purchase of Japanese eyewear brand Owndays, followed by its foray into Europe last month via a ₹407 crore acquisition of Spanish label Meller.

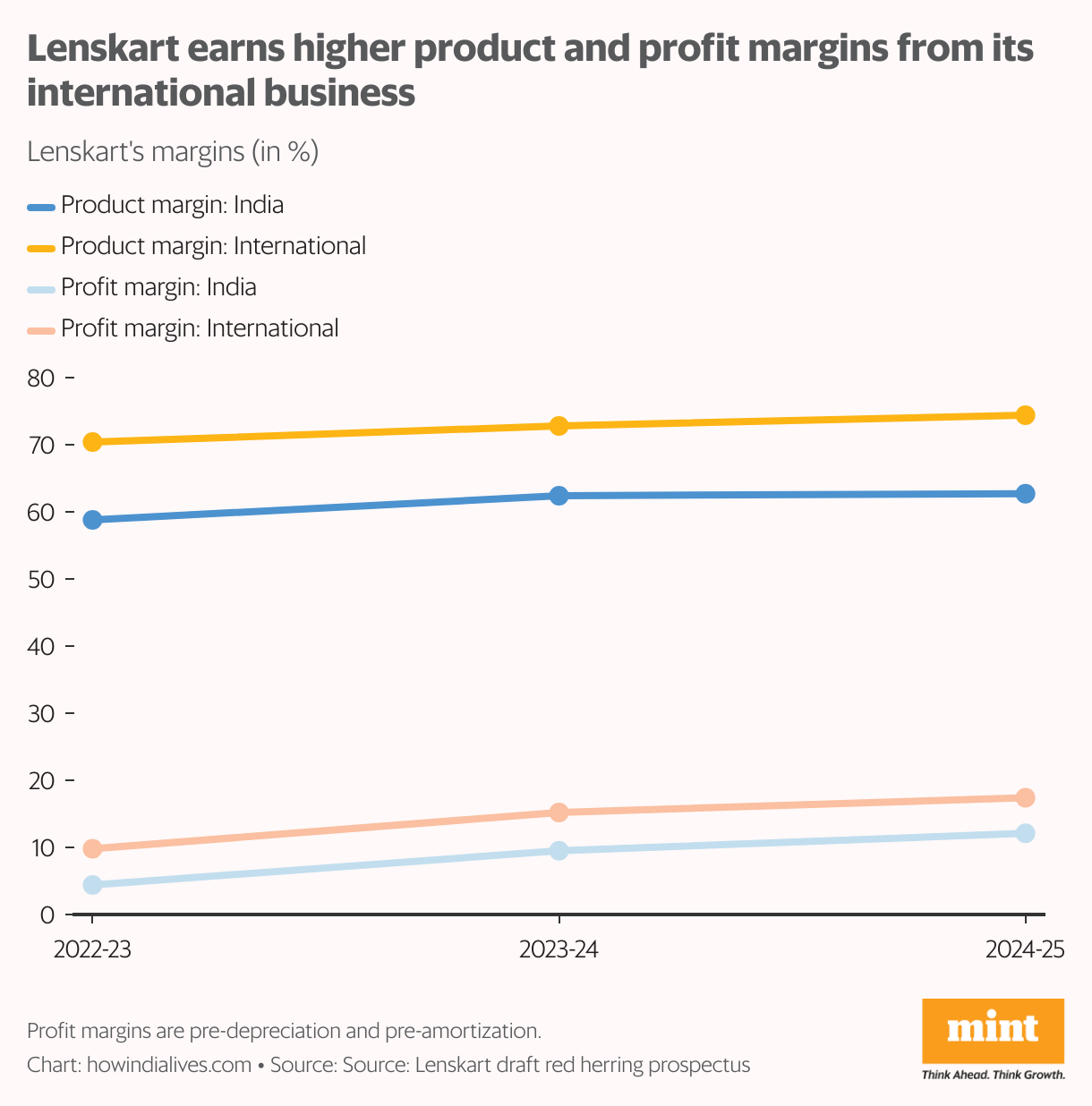

Unlike peers such as Zomato or Ola, which have scaled back their international bets, Lenskart has sustained a strong overseas presence. By FY25, nearly 40% of its revenues came from outside India.

Notably, its international operations are more profitable: while domestic product margins stood at 63%, overseas margins were higher at 74%. Even after accounting for marketing and commissions, operating margins landed in the 12–17% range.

Stores: New look

As it seeks to expand its store count further, these expense heads will keep margins under pressure.

Lenskart’s draft prospectus pegs its store footprint in India at 1.65 million sq. ft—over 2.3 times that of its closest organized rival in prescription eyewear. While its store fronts have multiple sizes, there is a brand consistency in look and feel.

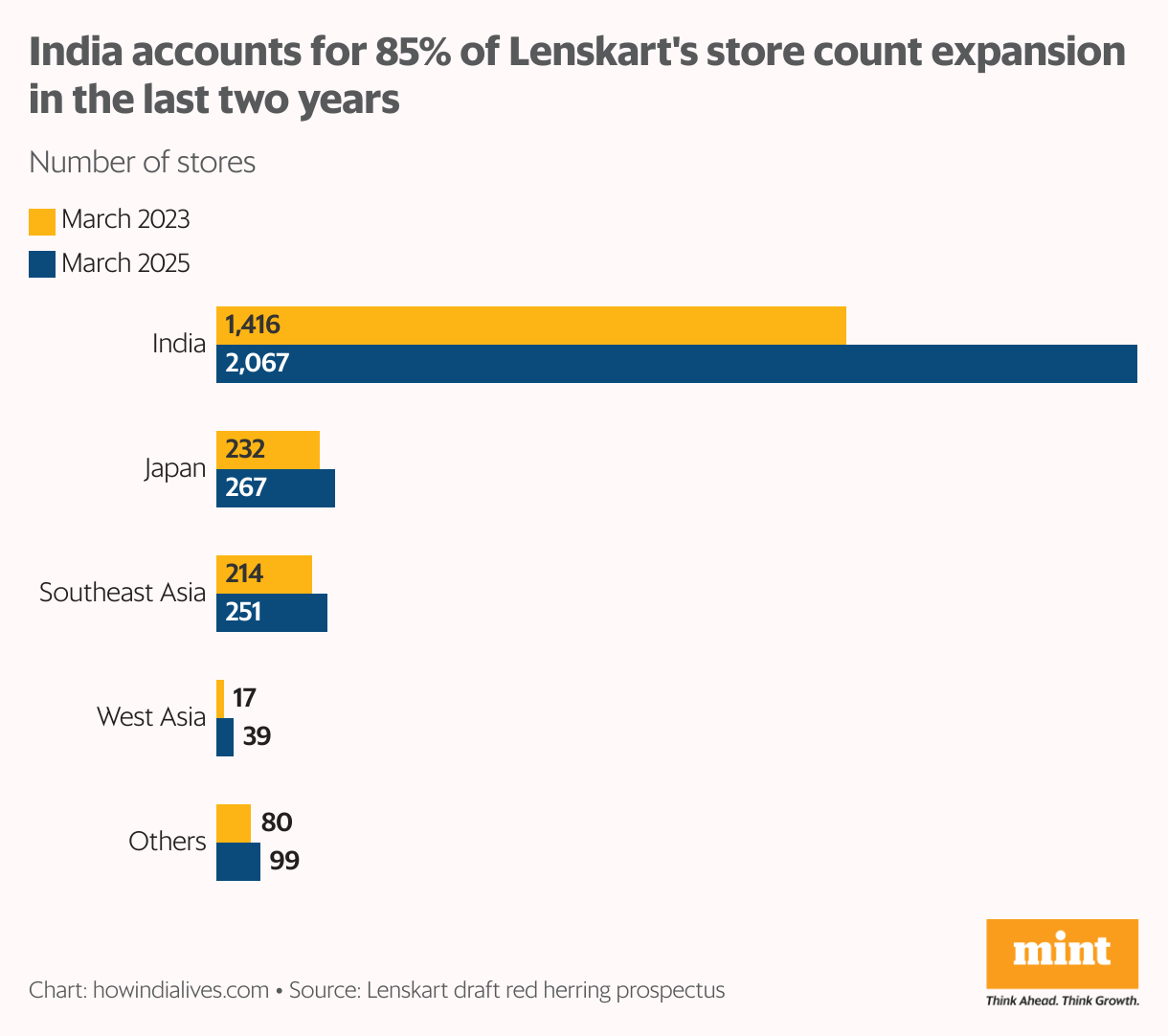

Between March 2023 and March 2025, Lenskart has increased its total store count from 1,959 to 2,723. Stores in India have accounted for 85% of this expansion. Titan Eye+, by comparison, has about 700 stores in India and seven outside India. In its proposed issue, Lenskart plans to raise fresh funds of up to ₹2,150 crore. Of this, it has earmarked ₹273 crore towards capital expenditure—store setup costs and additional equipment—for about 620 new stores by March 2029.

Demand: Looking beyond

Lenskart divides its India business into three markets: the eight metros, where it runs 900 stores; 39 Tier-I cities with 469 stores; and Tier-II and smaller towns, where it operates 698 outlets.

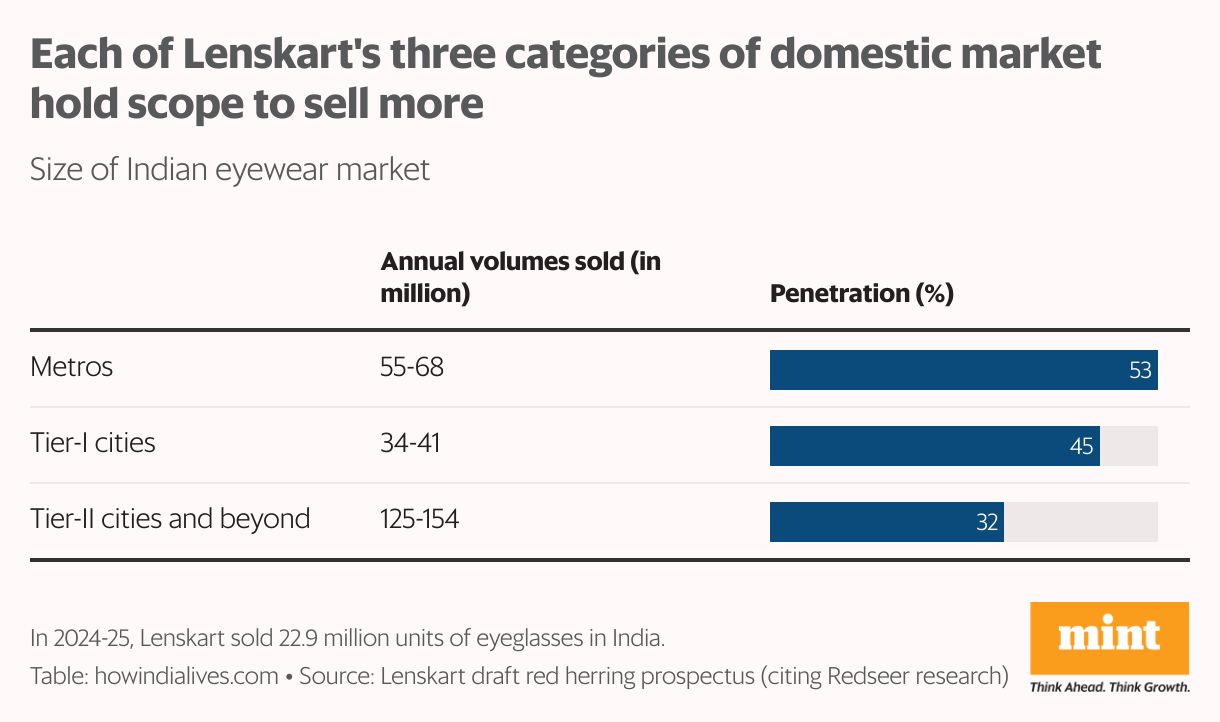

The numbers suggest ample headroom to expand across all segments. According to a Redseer report cited in its draft prospectus, India sells 214–263 million eyeglasses annually.

In FY25, Lenskart sold 22.9 million units—just about 10.7% at the lower end of the market size, underlining its modest share. Redseer also flagged a large unmet need: with penetration at only 32–53%, millions who require vision correction still go without glasses—a gap Lenskart hopes to close.

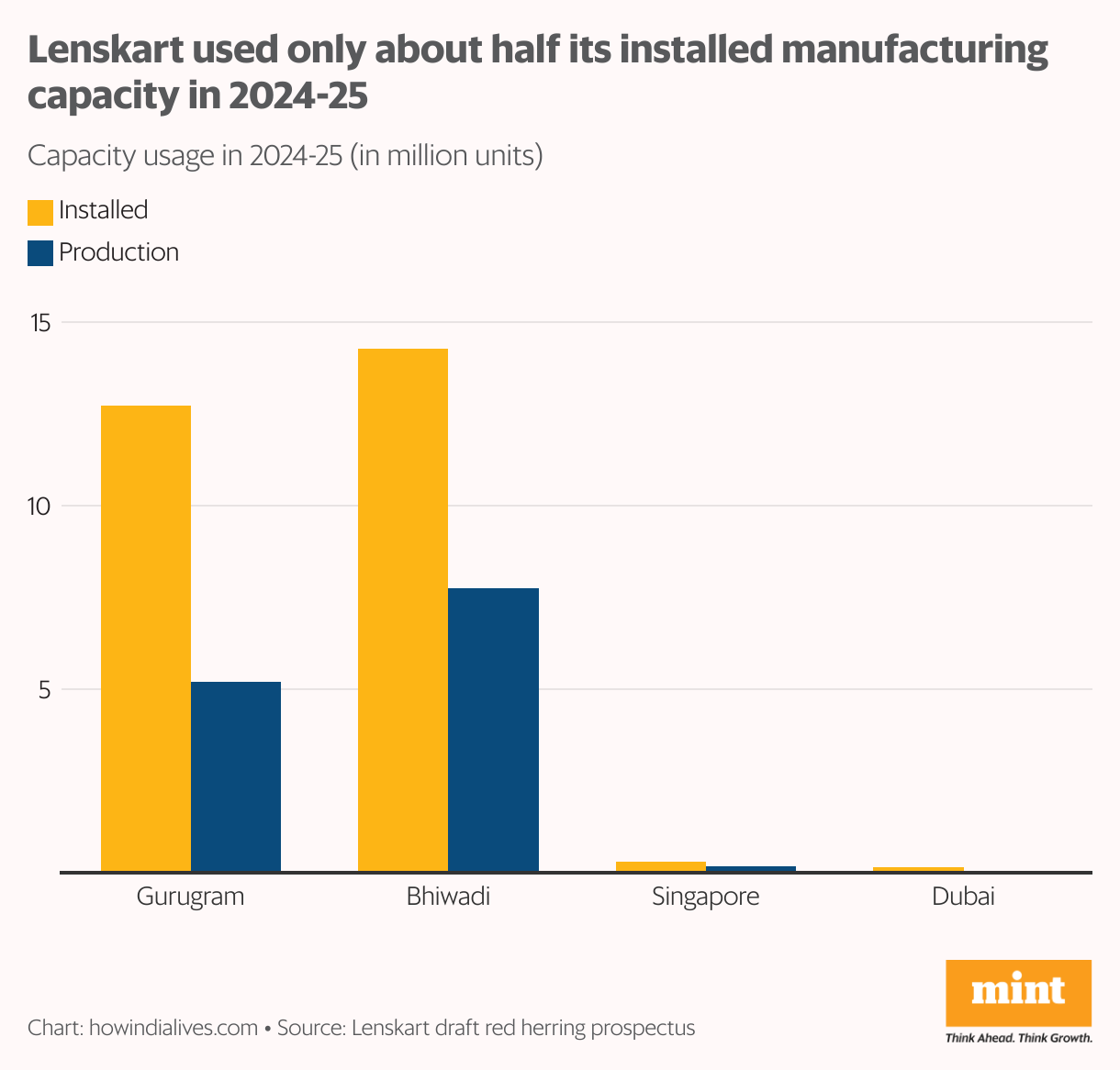

Manufacturing: Vertical integration

The risk for Lenskart is its expansion running way ahead of demand or an inability to draw incremental sales. It is investing a lot in every aspect of the business—from stores to manufacturing capacity, from foraying into new markets to acquiring new brands. A lot of this is in the physical space—after all, stores accounted for 76% of Lenskart’s eyewear bookings in India and 97% internationally.

Lenskart also has four manufacturing plants: in Gurugram and Bhiwadi in Haryana, Singapore, and Dubai. All of them operated far from capacity in 2024-25, clocking a combined utilisation of just 48%. Yet, the company is investing ₹1,500 crore in a new facility in Telangana. One reading of this is that Lenskart is confident of its integrated business model and growth prospects. But if business growth doesn’t keep pace with all the building, it could come back to bite Lenskart.

www.howindialives.com is a database and search engine for public data

#Lenskart #crafted #vision #eyewear #sector